Your phone rings late. It's a number you don't know. A voice on the other end says your son, husband, brother, or friend is in jail somewhere in Southern California, and bail has been set. Your heart drops. You start searching for loans for bail bonds because you need one answer right now. How do I get them out fast without wrecking my finances?

That panic is normal. Families make rushed decisions in these first hours, and that's exactly when bad financing choices happen. Some options are straightforward. Some are expensive. Some aren't really loans at all, even when they're advertised that way.

What you need is plain English. No sales language. No legal jargon. Just the difference between a bail bond payment plan and a true loan, plus what works in California when the clock is running.

Table of Contents

- The Urgent Search for Bail Money in California

- Understanding Bail Bond Premiums vs Traditional Loans

- Comparing Your Practical Financing Options

- The High Risks of Payday, Title, and Pawn Loans

- How California Bail Agency Payment Plans Work

- Your Step-by-Step Action Plan for Securing Bail

- Conclusion The Fastest and Safest Path to Release

- Frequently Asked Questions About Bail Financing

- Will co-signing for a bail bond affect my credit score

- What happens to my collateral after the case is over

- Can I get a bail bond with no money down at all

- What's the difference between state, federal, and immigration bonds

- Is a personal loan ever a good idea for bail

- Should I use a credit card instead of a bail agency payment plan

- How do I know if a payment plan is fair

The Urgent Search for Bail Money in California

A lot of families in California start the same way. Someone gets arrested in Ventura, Oxnard, Santa Barbara, Los Angeles, or another Southern California county. You hear a few scattered facts. A jail name. A charge you don't fully understand. Maybe a booking number if you're lucky. Then someone says the word “bail,” and suddenly you're trying to solve a financial problem you never planned for.

In that moment, people do what anyone would do. They search for fast cash. They ask relatives for help. They wonder if a credit card will work. They search for “no money down” offers and hope it's that simple. Sometimes it is. Often it isn't.

This is a common problem, not a strange one

The bail bond business is large because this situation happens every day. The U.S. Bail Bond Services market is projected at $3.5 billion in 2026, with 20,886 businesses operating in the sector in 2025, according to IBISWorld's bail bond services industry report. That matters for one reason. Bail financing isn't some obscure back-alley arrangement. It's a standardized financial service built around pretrial release.

The same report notes that the typical nonrefundable premium is about 10% of the total bail. That means the first number you need to focus on usually isn't the full bail amount. It's the premium needed to get a bond posted.

When a family panics, they often chase the full bail amount first. In many cases, that's the wrong number to focus on.

Why bad decisions happen fast

Pressure causes tunnel vision. You want your person out, and you want that solved in minutes. That's exactly why families sign the wrong financing agreement, misunderstand the co-signer obligation, or accept a flashy “1% down” ad without asking who qualifies.

If you stay calm for the next few minutes and understand the structure, you'll make a much better decision. Speed matters. So does knowing what you're buying.

Understanding Bail Bond Premiums vs Traditional Loans

The biggest misunderstanding I hear is this. People say they need a loan for a bail bond, when what they usually need is a way to pay the bail bond premium.

A bail bond is not a traditional loan. It's a surety contract. The indemnitor pays a non-refundable premium, typically 10% of the total bail, and the bond company guarantees the full amount to the court. If the defendant misses court, the surety can seek reimbursement from the indemnitor. That structure is explained clearly in this overview of how bail bond financing works.

Think of it like a premium, not a cash advance

The cleanest analogy is insurance. You pay a premium for the company to take on risk. You are not borrowing the full bail amount and then paying it back like a regular installment loan. You are paying a fee for the bond company to guarantee the court that the defendant will appear.

That distinction matters because families often expect the money to “come back” later. The premium does not come back. It is the cost of the service.

If you're trying to understand what bond amount leads to what premium in local cases, this guide on how much bail costs in Ventura and Santa Barbara County bail bonds gives a practical local breakdown.

What you are actually paying for

A bond company does more than front paperwork. The company is taking legal and financial risk on the defendant's court appearance. That's why the contract may also involve:

- A co-signer who agrees to be financially responsible

- Collateral in larger or riskier cases

- Court compliance requirements so the defendant appears as required

- Reimbursement exposure if the defendant fails to appear

Practical rule: If you're paying a bail agency, assume the premium is the service fee and ask separately whether any financing charges apply to the payment arrangement.

Where people get confused

The phrase Loans for bail bonds gets used loosely online. Sometimes it means a personal loan from a bank or online lender. Sometimes it means a credit card. Sometimes it means the bail agency lets you pay the premium over time.

Those are not the same thing.

One is a consumer debt product. One is revolving credit. One is a premium payment arrangement tied directly to the bail service. If you don't separate those three in your mind, it's very easy to compare the wrong costs and sign the wrong agreement.

Comparing Your Practical Financing Options

When a loved one is in jail, the “best” financing option is usually the one that gets the bond posted quickly without creating a second emergency next month. That means you need to judge options by speed, approval, total cost, and what you're risking personally.

What matters in a bail emergency

A personal loan might look cheaper on paper. A credit card might be familiar. A bail agency payment plan might be fastest. The right answer depends on what you can qualify for immediately and what the terms really say.

If a co-signer is involved, read this local explanation of how co-signing a bail bond works before you agree to anything. Co-signing is not symbolic. It creates real responsibility.

Bail Financing Options Compared

| Financing Method | Typical Speed | Cost & Interest | Approval Likelihood | Key Risk |

|---|---|---|---|---|

| Bail agency payment plan | Usually fast because it's handled alongside the bond process | May be simpler than outside borrowing, but you must ask about every fee and payment term | Depends on case details, co-signer strength, income, residency, and sometimes collateral | Missing payments or violating bond terms can create bigger problems fast |

| Personal loan | May take longer than a direct bail arrangement, depending on lender and documentation | Can be lower-cost than other borrowing in some situations, but only if terms are clean and approval is quick | Depends heavily on credit, income, and lender underwriting | You may lose time applying and still not get funded fast enough |

| Credit card | Fast if you already have available credit | Can become expensive quickly through interest and cash-advance style charges, depending on how used | Works only if you already have room on the card | High balances can strain your finances long after release |

My direct recommendation

Start with the bail agency first, not the lender. That sounds backward to people who are used to shopping for financing before shopping for service. In a bail situation, it isn't backward. It's efficient.

The agency can tell you the actual premium, whether a payment plan is even available for that case, what co-signer profile is needed, and whether collateral would solve the problem faster than a loan application. If you run to a bank or online lender first, you may waste valuable time solving the wrong problem.

The option families underestimate

Credit cards are common because they're immediate. But they're blunt instruments. They don't explain the release process, they don't verify booking details, and they don't help you understand the co-signer agreement. They just shift the stress into monthly statements.

A payment plan through a bail agency is usually more practical when the agency can evaluate the case and move on paperwork at the same time. A personal loan only makes sense if you can qualify quickly, understand the repayment terms, and know for sure it won't delay release.

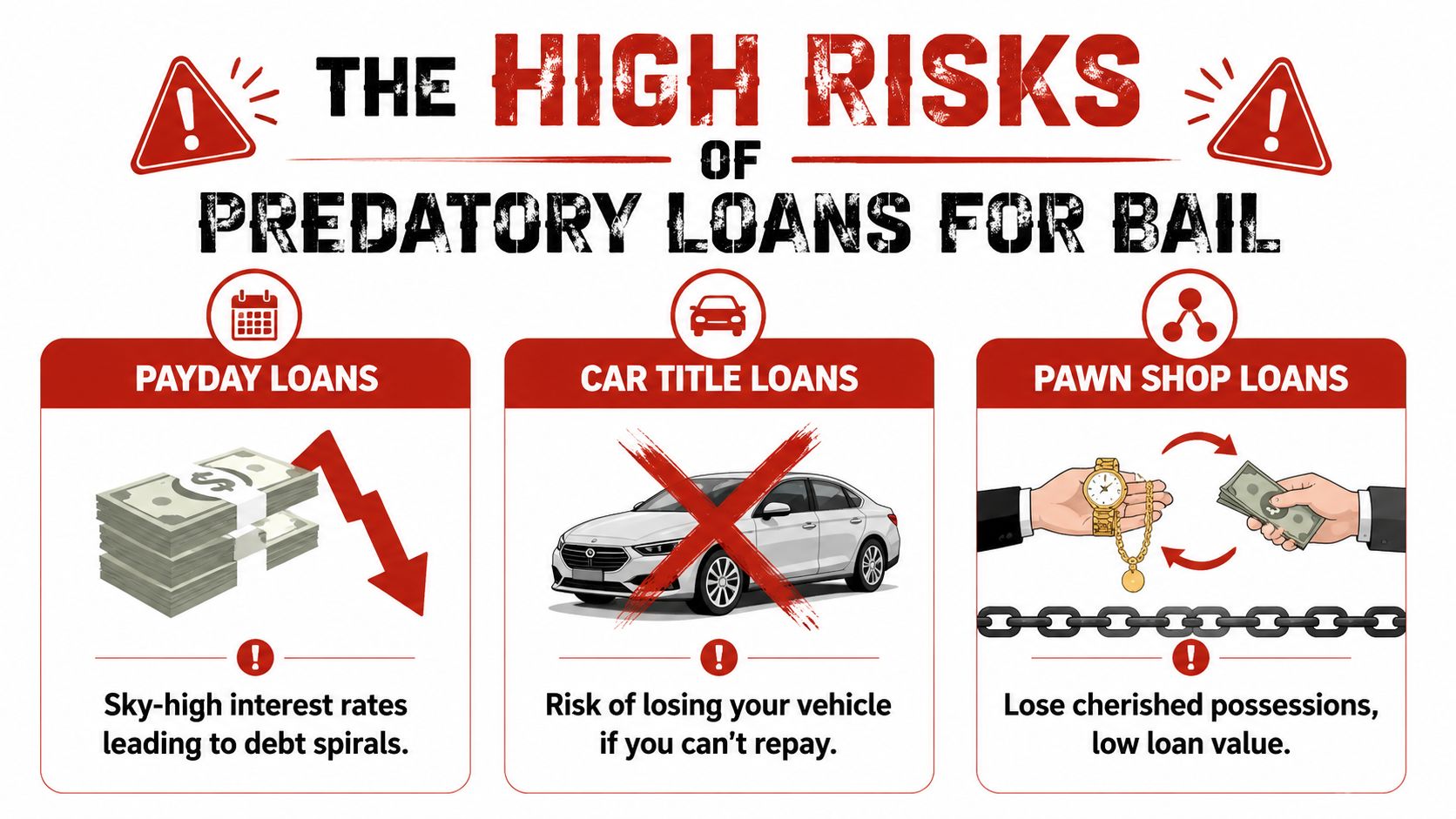

The High Risks of Payday, Title, and Pawn Loans

If you are desperate, payday, title, and pawn loans will look tempting. Don't confuse fast approval with a safe decision. These products are built for people under pressure, and a family dealing with an arrest is exactly the kind of customer those lenders target.

Why these loans trap families

Loan-like bail funding is often priced like short-duration, high-risk consumer credit. One example from AmOne's discussion of posting bail with a personal loan notes that even a 10% premium used for only a couple of months can imply a cost around 60% APR, and repayment plans that stretch to 12 months can raise total cost further through interest and fees.

Now add a payday lender or title lender on top of that kind of pressure, and you can see the problem. You are no longer solving one emergency. You are stacking emergencies.

A title loan puts your vehicle on the line. For many California families, that vehicle is how they get to work, pick up kids, and handle court appearances. Losing it over a short-term bail panic is a brutal trade.

Warning signs to walk away from

If any lender uses pressure, vagueness, or speed as a substitute for clarity, back up. Fast money is not the same as fair money.

- Unclear payoff terms. If they can't explain exactly what you'll owe and when, don't sign.

- Asset seizure risk. If your car title, jewelry, or keepsakes are at stake, treat that as a last resort, not a convenience.

- Short repayment windows. The shorter the window, the easier it is to fall behind.

- Pressure to sign immediately. You need a clear agreement, not a countdown clock.

A family can recover from the shock of an arrest. Recovering from a bad title loan is often much harder.

Pawn loans are usually the weakest option of the three. You give up something valuable, get less than it's worth, and still may not solve the full bail problem. That's not financing. That's loss management in a panic.

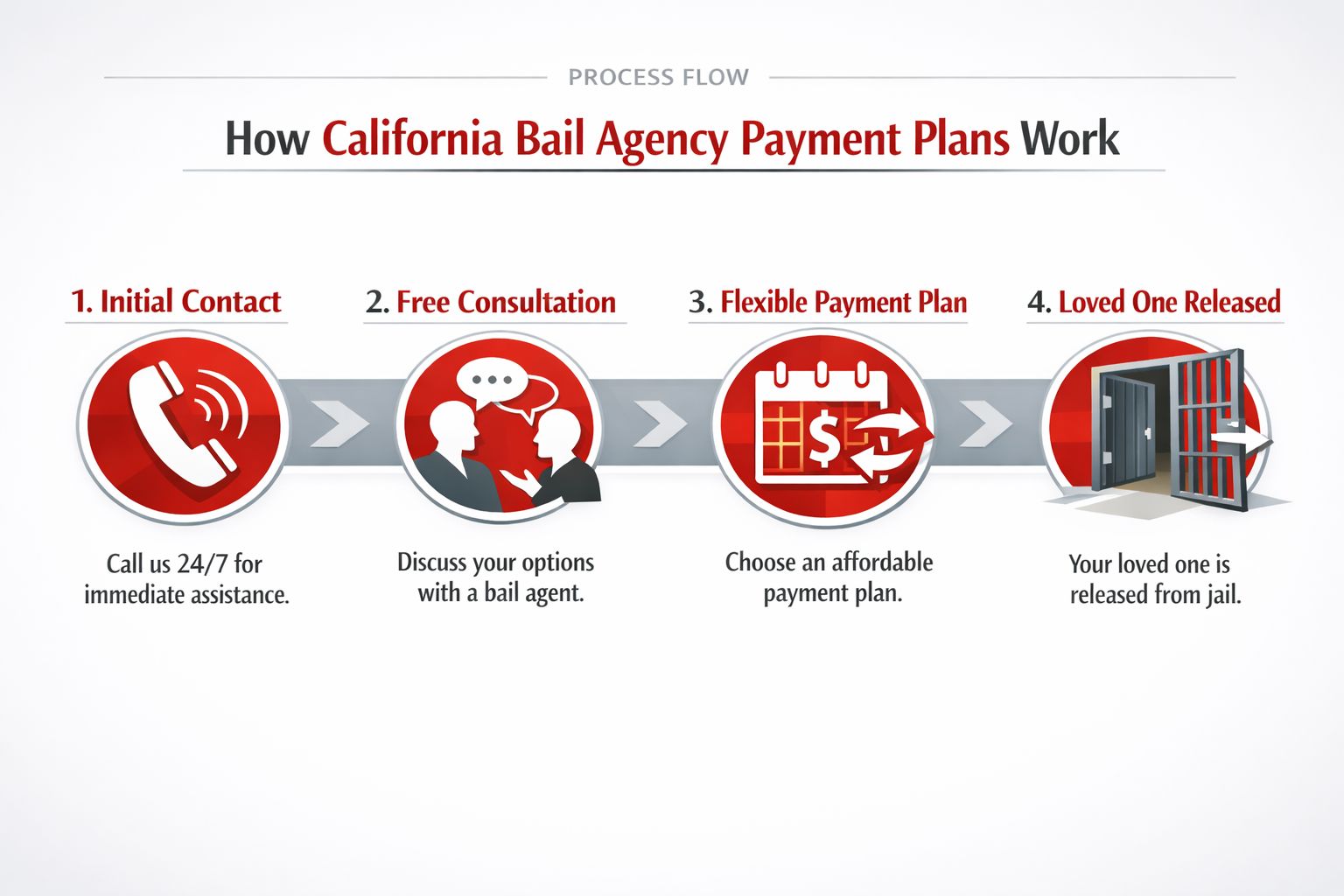

How California Bail Agency Payment Plans Work

Your loved one is sitting in jail, someone online is shouting “1% down,” and it sounds like a loan. In California, it usually is not. A bail agency payment plan is an agreement for paying the bail bond premium over time. A true loan is a separate credit product with its own underwriting, interest, and credit consequences.

What a payment plan really is

That difference matters.

With a bail agency payment plan, the agency is deciding whether to post the bond and let you pay the premium in installments. With a true loan, a lender gives you money and expects repayment under a separate credit agreement. Those are two different transactions, and families get burned when they treat them like the same thing.

As explained in this California-focused breakdown of bail bond financing, many “1% down” offers are premium financing plans tied to the bond, not standard consumer loans. Approval can depend on the defendant's situation, the co-signer's strength, residency, timing of the arrest, and the type of case. Some case types are excluded entirely.

So ask the blunt question first. “Is this a bail bond payment plan, or are you sending me to a lender?”

If you want to see how a local agency lays out terms, review these Ventura County bail bond payment plan options.

Who usually gets approved

California bail agencies look at risk fast. They are not only asking whether you can make a first payment. They are deciding whether the bond should be written at all, whether the co-signer is reliable, and whether the defendant is likely to show up in court.

Expect requests for ID, proof of income, proof of residence, employment details, and information about the defendant's local ties. A stronger co-signer can matter as much as cash. On larger bonds, collateral may come up. That can include property, a vehicle, or something else the agency can verify and document.

Here is the practical filter to use during that call:

- Ask exactly what you must pay today

- Ask how many payments you will have, and on what dates

- Ask whether the plan reports to credit bureaus or involves a lender

- Ask what collateral, if any, is being pledged

- Ask what happens if the defendant misses court

- Ask whether the charge or bond type is excluded from payment plans

Why families should call the agency before applying for a loan

Start with the bail agency. That is the fastest way to find out whether you even need outside financing.

A direct payment plan keeps the release process and the payment arrangement in one place. The agency can verify booking details, confirm whether the bond is eligible, tell you what the co-signer needs, and explain any collateral requirement in the same call. That saves time, and time matters when someone is waiting in custody.

Bada Bing Bail Bonds is one example of an agency that may discuss those terms directly instead of pushing you straight toward a separate lender.

Here is my advice. If the agency can write the bond with a clear payment plan, take a hard look at that before you apply for a true loan. A loan can trigger a credit check, add another contract, and create another monthly bill after the court case is already stressing your family. A payment plan is not automatically cheap or easy, but it is often simpler, faster, and less risky than stacking a new loan on top of an arrest.

Your Step-by-Step Action Plan for Securing Bail

When people are scared, they need a checklist. Not theory. Not slogans. Just the next move.

What to do first

Confirm the jail and booking details.

Get the full legal name, date of birth if available, booking number if available, and the exact jail location. Wrong information wastes time.Verify the bail amount before chasing money.

Don't rely on a frantic text from a friend of a friend. Get the actual amount tied to the booking.Call a local bail agent before applying for outside financing.

A local agent can usually tell you faster whether the case qualifies for a payment plan, a co-signer arrangement, or collateral. This guide on how to bail someone out fast is a useful reality check on how the process moves.Understand the co-signer role.

If you sign, you are not just helping emotionally. You may be taking on financial responsibility and promising cooperation if the defendant fails to appear.

Don't sign anything until you can answer this question clearly: “If my loved one misses court, what exactly am I responsible for?”

If you do not qualify right away

Some co-signers won't qualify for low-down-payment plans. That's common. It can happen because of income, weak credit, missing documents, or the size and risk of the bond.

In those situations, collateral may be the fallback. As noted in this overview of options for people who do not qualify for standard bail financing, some agencies allow property or other assets instead of a cash down payment. That option gets ignored online, but in real cases it can be what makes release possible.

A few practical questions to ask right away:

- Can collateral replace part of the cash requirement

- What documents are needed for the asset

- When is collateral returned after the case ends

- Who must sign if the asset is jointly owned

That's your backup plan if the low-down-payment ad doesn't apply to your case.

Conclusion The Fastest and Safest Path to Release

Families searching for Loans for bail bonds usually think the first problem is borrowing money. In California, that's often not the actual first problem. The actual first problem is understanding whether you need a true loan, a premium payment plan, a co-signer, or collateral.

That distinction saves time and prevents expensive mistakes.

A payday lender won't guide you through the jail process. A title lender won't explain bond obligations. A generic online loan form won't tell you whether the case even qualifies for the financing you thought you needed. A local bail agency can answer those questions right away.

So my advice is simple. Don't start with the flashiest financing ad. Start with the actual bond process. Verify the booking, learn the premium, ask about payment plan eligibility, and get clear on co-signer risk before you touch outside credit.

That's usually the fastest path to release, and it's almost always the safer one.

Frequently Asked Questions About Bail Financing

Will co-signing for a bail bond affect my credit score

Not automatically. A bail bond co-sign is not the same thing as opening a standard consumer loan account with a normal lender. But if the agreement includes financed payments and you fail to pay, the consequences can become financial very quickly. The smart move is to ask one direct question before signing: how are missed payments handled, and does the agreement involve any reporting, collections, or enforcement steps?

What happens to my collateral after the case is over

If the defendant meets all court obligations and the bond is properly concluded, collateral is generally returned according to the agreement. The key word is “properly.” Read the paperwork and ask what conditions must be satisfied before release of collateral. Ask who must sign off, what timeline applies, and whether any costs can be deducted if the defendant caused enforcement problems.

Can I get a bail bond with no money down at all

Sometimes, but don't assume you will. Many ads use low-down-payment language broadly, while actual approval depends on the case, the co-signer, the timing of the arrest, and whether the defendant fits the agency's risk standards. In California, the headline offer is often far narrower than the ad makes it sound.

What's the difference between state, federal, and immigration bonds

They are not interchangeable. State cases usually follow the local county process most families think of when they hear “bail bond.” Federal and immigration matters often involve different rules, different approval standards, and different financing availability. Some agencies do not offer payment plans for those case types at all. That's why you should ask about case type first, before discussing down payment.

Is a personal loan ever a good idea for bail

It can be, but only under specific conditions. It needs to fund fast enough to matter, and the repayment terms need to be clean enough that you are not creating another emergency after release. If the personal loan process is slow, uncertain, or full of fees, it defeats the point.

Should I use a credit card instead of a bail agency payment plan

Only if it solves the problem better. A credit card may be immediate if you already have available credit, but it doesn't help you understand the bond terms, co-signer responsibility, or local release process. Families often use cards because they feel familiar, not because they are the smartest option.

How do I know if a payment plan is fair

Ask for the full breakdown in plain English. What is due now. What is due later. What happens if a payment is missed. Whether collateral is involved. Whether the plan changes based on charge type or county. If the answers are vague, keep asking.

For more plain-English answers to common concerns, read these California bail bonds FAQ straight answers.

If you need help sorting out bail financing in Ventura, Santa Barbara, Los Angeles, or nearby Southern California counties, contact Bada Bing Bail Bonds. A licensed agent can verify booking details, explain the premium and co-signer obligations in plain English, and tell you whether a payment plan or collateral option is available for your specific case.