The call usually comes at the worst time. Late at night, little information, a scared voice on the other end, and one question that matters more than anything else: how do we pay to get them out?

In Southern California, families often lose time because nobody explains the payment side clearly. They hear a bail amount, assume they need the whole thing in cash, and start calling relatives in a panic. That's usually not how the process works. If you need a quick plain-English refresher on the basics first, this overview of what bail means in California is a good place to start.

What matters right now is simple. You need to know what the actual cost is, what forms of payment are usually accepted, when a payment plan makes sense, when collateral might come into play, and what paperwork will slow things down if you don't have it ready.

Table of Contents

- Your Guide to Bail Bond Payment Options in a Crisis

- The 10 Percent Rule in California Bail Bonds

- Comparing Your Primary Payment Methods

- Flexible Options When You Need Them

- Using Assets for Large or High-Risk Bonds

- Your Step-by-Step Guide to Paying for a Bond

- Common Questions and Red Flags to Avoid

Your Guide to Bail Bond Payment Options in a Crisis

If you're reading this after a booking call from Ventura, Oxnard, Santa Barbara, Van Nuys, or downtown Los Angeles, you're probably trying to make decisions with incomplete information. That's normal. Most first-time callers don't know the jail's release timing, don't know whether the bail amount is final, and don't know whether a card, cash, or co-signer will get the bond moving fastest.

The first practical move is to stop guessing and gather the basics. You need the full name of the person in custody, their date of birth if you have it, where they were booked, and any booking number or case information you were given. Once that's verified, the payment discussion gets much easier because the bond amount, risk level, and paperwork needs are tied to the actual booking record, not rumors from friends or social media.

Practical rule: The fastest families aren't always the ones with the most money. They're the ones who get accurate booking details first and choose a payment method that can clear without delay.

In California, the main issue usually isn't whether some payment option exists. It's whether that option will hold up under time pressure at night, over a weekend, or during a holiday release window.

Here's what people usually need help sorting out right away:

- Total cost vs. upfront cost: Many callers hear the bail amount and think they must produce the full court amount immediately.

- Accepted payment type: Some methods are convenient but not ideal for rapid jail processing.

- Plan eligibility: Not every case is a fit for an installment arrangement.

- Co-signer responsibility: A family member may need to sign, and that person needs to understand the risk before agreeing.

- Collateral questions: For larger bonds, the issue may be less about monthly affordability and more about security.

When a family gets calm, clear answers on those five points, the whole situation usually becomes manageable.

The 10 Percent Rule in California Bail Bonds

The first number most families need to understand is not the full bail amount. It's the premium.

What you're actually paying for

In the U.S., the most common commercial bail bond structure is a nonrefundable fee of about 10% of the total bail, and the Bureau of Justice Statistics gives the practical example that a $10,000 bail can mean about a $1,000 payment to a surety company through a commercial bond arrangement, as explained by the Bureau of Justice Statistics overview of bail.

That's the key distinction. You are not usually handing the bondsman the full bail amount. You're paying the premium for the bond service, and the bond company posts the surety bond.

Much confusion is eliminated once families understand this: the premium is more like the cost of obtaining the bond, not a deposit you get back later. If the defendant appears as required, that does not convert the premium into a refundable payment. It's still the fee for the service.

If you want a more detailed walk-through of that structure, this breakdown of how bail bonds work in California helps put the mechanics in plain English.

Why families get confused

The stress usually comes from mixing up two different paths:

- Paying the court directly

- Using a bail bond company

Those are not the same transaction. Direct court payment can involve different rules. A commercial bond usually means paying the premium and completing the required paperwork so the bond can be posted.

Families often waste the most time trying to raise the full bail amount when the immediate decision is really whether they can handle the premium and any related underwriting requirements.

In California practice, transparency matters. If an agency is discussing the premium, payment timing, collateral, and co-signer terms clearly, you can evaluate the deal. If they're vague, rushing you, or talking around the paperwork, slow down and ask direct questions.

Three questions should be answered clearly before you agree:

- What is the premium amount?

- Is that premium nonrefundable?

- Are there any add-on charges beyond the standard bond paperwork and approved payment arrangement?

If you don't get straight answers to those three questions, keep calling.

Comparing Your Primary Payment Methods

Once the premium is clear, the next issue is how to pay it in a way that won't create delays.

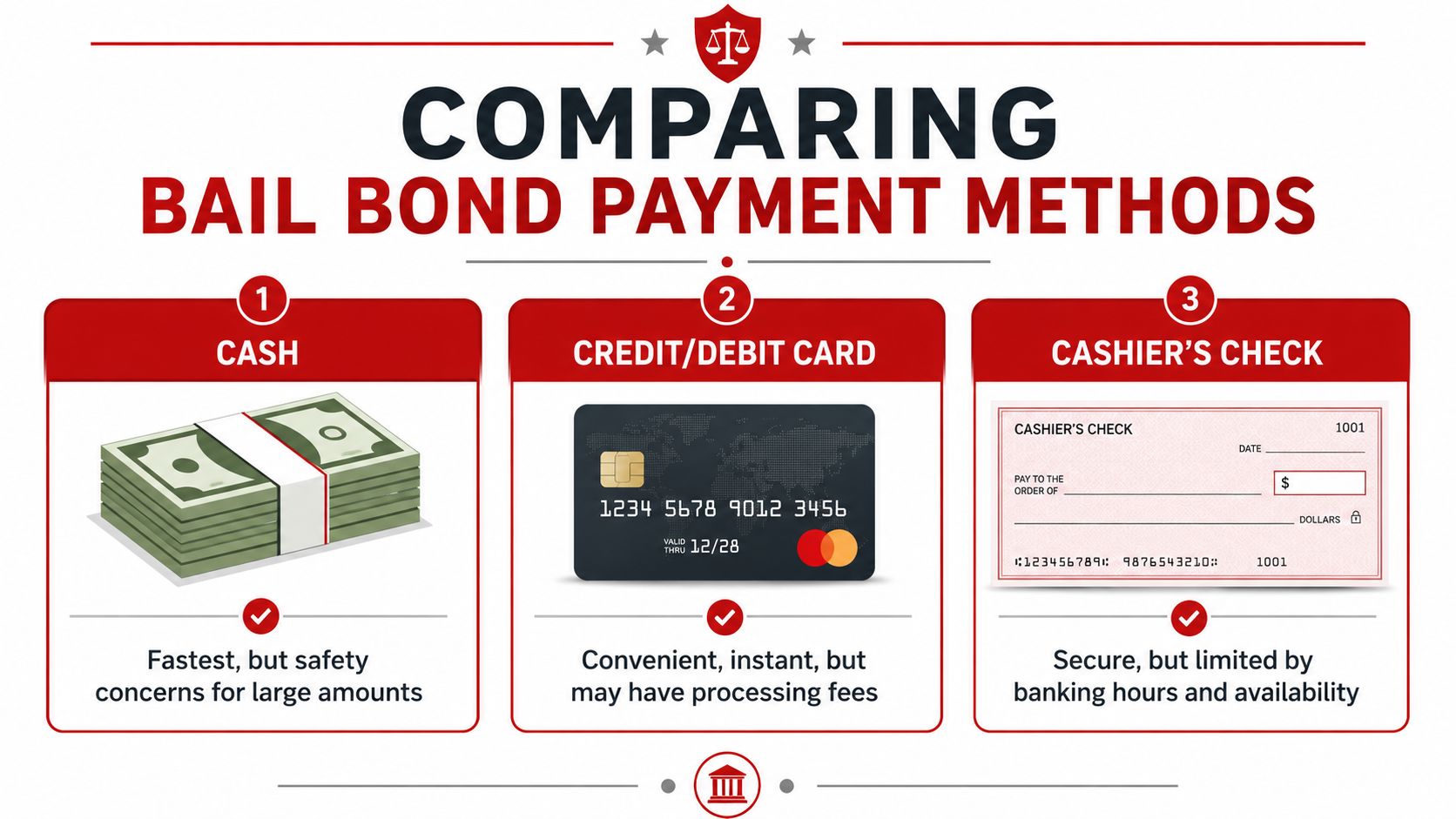

What gets processed fastest

Accepted bail-bond payment rails are usually limited to cash, cashier's checks, major credit/debit cards, and money orders, with collateral sometimes used for larger bonds. The practical reason is settlement and chargeback risk, and sources note that cash and cashier's checks are fastest for release processing, while card acceptance is less universal, as explained in this guide to bail bond payment options and accepted payment rails.

That lines up with what families run into in real life. The fastest payment method is often the one with the fewest verification issues.

Here's the short version:

- Cash works well when you already have the funds and can get them to the office safely.

- Debit or credit card can be convenient, especially in the middle of the night, but card acceptance varies and some transactions trigger extra review.

- Cashier's check is reliable, but it depends on banking access, which can be a problem after hours.

- Personal checks are usually a bad fit in a crisis because verification and collection timing don't match the urgency of a jail release.

Bail Bond Payment Method Comparison

| Payment Method | Speed of Release | Convenience | Best For |

|---|---|---|---|

| Cash | Usually very fast once delivered | Less convenient for large amounts | Families with immediate access to funds |

| Credit or debit card | Can be fast if accepted and approved | Very convenient, especially after hours | Callers who need to handle payment remotely |

| Cashier's check | Often fast once obtained | Less convenient outside banking hours | People who want a bank-backed payment method |

A few practical trade-offs matter more than people expect.

- Cash: Good for speed, but carrying a large amount at night isn't ideal. Families also sometimes overfocus on cash when a remote card payment would be safer and faster overall.

- Card: Good for convenience. The catch is that not every agency wants chargeback exposure, so you need to confirm acceptance before assuming it will work.

- Cashier's check: Solid when the bank is open and nearby. Not so helpful when the arrest happens late and every branch is closed.

If release speed matters, choose the payment method that can actually be completed right now, not the one that looks best on paper.

The right question is not “What's the best payment method?” It's “Which payment method can clear cleanly tonight?”

Flexible Options When You Need Them

Not every family can pay the full premium in one shot. That doesn't automatically end the conversation. It means the discussion shifts to timing, qualification, and who is willing to stand behind the bond.

How payment plans usually work

In major U.S. bail markets, the premium is typically structured as a non-refundable 10%–15% fee, and payment plans mainly change the timing of collection rather than the legal character of the premium. Some sources also note that agencies may require an upfront down payment of 10%–20% and recurring automatic payments to reduce default risk, according to this explanation of how bail bond payment plans are commonly structured.

That distinction matters. A payment plan usually doesn't turn the premium into something refundable. It spreads part of the obligation over time.

Families should ask these questions before agreeing to any installment setup:

- How much is due today?

- What are the scheduled follow-up payments?

- Is the plan interest-free, or is it a financing arrangement with added cost?

- Will automatic payments be required?

- What happens if a payment is missed?

A local option that states it offers payment plans for Ventura County bail bonds may be useful if you're trying to understand what documents and approval details are typically requested in California.

Most agencies look for signs that the plan is workable. Stable income, a reachable co-signer, valid identification, and a realistic payment path all help. What doesn't work is vague promises, missing documents, or a co-signer who doesn't understand what they're signing.

Here's a quick overview that can help before you call:

- Best fit for plans: Families with reliable income but limited cash on hand tonight.

- Worst fit for plans: Cases where nobody can document income, identity, or a responsible co-signer.

- Common mistake: Focusing only on the monthly number and not on the total obligation or default terms.

Before deciding, it helps to hear the process explained in a simple format:

What a co-signer is agreeing to

A co-signer is not just providing moral support. That person is taking on legal and financial responsibilities tied to the bond agreement.

In plain terms, the co-signer usually agrees to do three things:

- Help ensure the defendant complies with court obligations.

- Remain responsible for the payment agreement if one exists.

- Accept the collateral consequences if security was pledged and the bond terms are broken.

The strongest co-signer is not always the closest relative. It's the person with stable contact information, clear judgment, and the willingness to stay involved until the case is over.

If someone is hesitating, that's not always a problem. It may mean they need the contract explained more carefully before they commit.

Using Assets for Large or High-Risk Bonds

Collateral is where many families get nervous, mostly because nobody has explained it clearly.

Collateral is not required in every case. It usually comes up when the bond is large, the risk profile is higher, or the agency needs security beyond the premium and co-signer promise.

When collateral comes up

Accepted payment setups may include collateral for larger or higher-risk bonds, and common collateral categories include vehicles, real estate equity, jewelry, or securities whose value must meet or exceed the bond exposure, with the agency holding that collateral until court compliance is complete, as outlined in this explanation of collateral and larger bail bond arrangements.

That means collateral is a security tool. It is not the same thing as the premium, and it is not automatically a sign that something is wrong with the case. It's a way for the bond company to manage the risk it takes on.

Common situations where collateral may be discussed include:

- Large bond exposure: The bond amount is high enough that the agency wants extra security.

- Limited liquid funds: The family can cover part of the obligation but not enough to support the full risk.

- Case-specific concerns: Prior failures to appear, unstable residence history, or limited co-signer strength can push the file into collateral territory.

What the collateral process looks like

A clean collateral process should be documented and understandable.

Expect the agency to ask for proof of ownership, identification, and supporting paperwork tied to the asset. For a vehicle, that might mean title documents. For real property, it usually means ownership documentation and equity review. For valuables, it may mean appraisal or verification.

Ask direct questions before signing:

- What asset is being pledged, exactly?

- Who holds the paperwork while the case is pending?

- What triggers return of the collateral?

- What would place the asset at risk?

The answer to the last question is the most important one. Families need to know that the asset is tied to compliance. If the defendant appears as required and the bond is properly exonerated at the end of the case, the collateral should be released back according to the agreement.

Your Step-by-Step Guide to Paying for a Bond

When the phone rings late and everyone is talking at once, the process feels harder than it is. The cleanest way through it is one step at a time.

What to have ready before you call

Have these items in front of you if possible:

- Defendant information: Full legal name and date of birth if known.

- Jail details: Booking location, booking number, or any citation/reference number you were given.

- Your identification: A valid government-issued ID for the person signing.

- Payment support documents: If you're asking for a payment plan, be ready with proof of income or employment and basic residence information.

- Co-signer information: If someone else will sign, get that person involved early instead of relaying messages back and forth.

If you're new to the signing side of the process, this guide on how co-signing a bail bond works in California helps clarify what the signer is agreeing to.

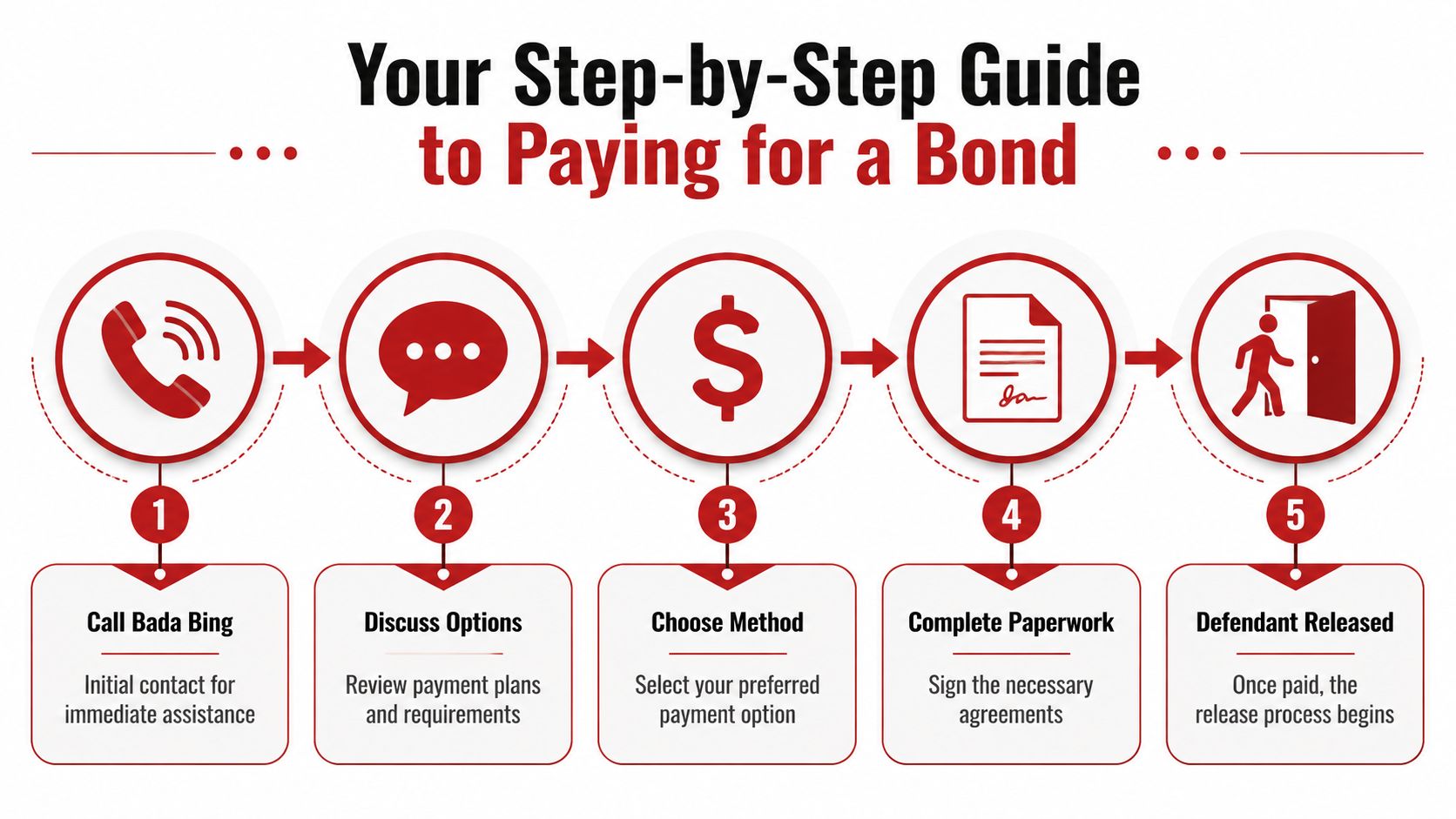

The payment and release sequence

Most California bail transactions follow a practical sequence like this:

Confirm the booking

The agent verifies that the person is in custody, where they are, and what bail amount or hold is showing. This step prevents wasted time and bad information.

Review the case basics

Charges, bail amount, and local jail procedures shape what payment options are realistic. Some jails move quickly. Others have release bottlenecks that matter just as much as payment timing.

Choose the payment route

The decision is made between immediate payment, a structured plan, co-signer support, or collateral-backed underwriting.

Complete the paperwork

Depending on the agency and the case, this may be done digitally or in person. Read everything. A rushed signature is where many misunderstandings begin.

Post the bond and wait on release processing

After the bond is accepted, the jail controls the physical release timeline. Payment gets the process started. It doesn't mean the doors open instantly.

If you want one straightforward example of a California agency workflow, Bada Bing Bail Bonds states that it verifies booking details, explains charges and payment options in plain English, and coordinates paperwork and jail posting across Ventura, Santa Barbara, Los Angeles, and nearby Southern California counties.

Keep one person in charge of communication. Families move faster when one signer, one backup contact, and one payment source are clearly identified.

Common Questions and Red Flags to Avoid

The last part of the decision is knowing what not to fall for.

Quick answers families ask at all hours

What happens if charges are dropped?

If you used a commercial bond, the premium is generally the fee for the service and is not returned just because the case ends favorably. That's one reason families should make sure they understand the contract before signing.

Should we finance the bond no matter what?

Not always. The bail-help options also include nonprofit and no-fee models in some situations, and some recent explainers point people toward bail reduction requests or supervised pretrial release instead of borrowing for a bond, as described by The Bail Project's help resources.

What if the defendant misses court?

That's serious. It can expose the co-signer and any pledged collateral to consequences under the bond agreement. If there's any confusion about a court date, handle it early, not after a missed appearance.

For a broader plain-English list, this California-focused bail bonds FAQ with straight answers covers many of the questions families ask right after release.

Red flags that should make you stop

Watch for behavior that signals trouble:

- Pressure before explanation: If someone wants a signature before clearly explaining premium, payment timing, and co-signer duties, slow the process down.

- Vague financing language: “Low payment” doesn't mean much unless you know the down payment, schedule, and whether extra financing cost applies.

- Unclear collateral terms: Never pledge an asset unless the agreement states what secures it and what returns it.

- No written answers: If promises aren't reflected in the paperwork, assume they don't exist.

The right agency won't make a hard night harder. They'll answer directly, explain the risk plainly, and give you a payment path you can complete.

If you need immediate help, Bada Bing Bail Bonds is available around the clock for Southern California bookings. Have the defendant's name, booking location, and your ID ready, and ask for the premium, accepted payment methods, co-signer requirements, and any collateral terms in plain language before you sign.