The phone rings late. A brother, daughter, husband, or friend says they've been arrested in Ventura, Oxnard, Camarillo, or somewhere else in Ventura County. The next words are usually rushed and hard to follow. Then comes the part that hits the family hardest. “They set bail.”

At that point, individuals aren't asking legal theory questions. They want one answer. How do we get them out, and what if we don't have enough cash sitting in the bank right now?

That's where collateral sometimes enters the conversation. In plain English, collateral is property or another asset used to secure the bail bond when the bond amount or risk level is too high for the bond to be written on signature and premium alone. Families calling about bail bonds Ventura or Ventura County Jail bail bonds usually want to know one thing about collateral. What works in real life, not just on paper.

If you're trying to move fast, start with the basics first. This guide on how to bail someone out fast walks through the first steps while emotions are still high and time matters.

Table of Contents

- That Urgent Call and the Question of Collateral

- Why Collateral Is Sometimes Required for Bail Bonds

- Assets Commonly Used for Ventura County Bail Bond Collateral

- How We Evaluate and Approve Your Collateral

- Safeguarding and Recovering Your Pledged Assets

- No Collateral? Other Options for Securing a Bond

- Frequently Asked Questions About Bail Bond Collateral

That Urgent Call and the Question of Collateral

A family in Ventura gets a call from the jail after midnight. Another one in Oxnard gets the same call before sunrise. The details are always a little different, but the pressure feels the same. Someone they care about is in custody, the bail amount looks impossible, and nobody in the room knows whether a bondsman will ask for cash, a co-signer, or property.

That's usually when the word collateral starts sounding more intimidating than it really is.

In the bail world, collateral isn't some unusual legal trick. It's a backup form of security. If the bond is large, the charge is serious, the booking history raises concern, or the defendant has a record of missing court, a bail agent may need something more than the premium payment before posting the bond. That doesn't mean the family did anything wrong. It means the agency is looking at risk the same way any secured lender would.

The practical question isn't just what can be used as collateral. It's what can be verified quickly, valued reasonably, and documented clearly enough to avoid slowing down release.

For families dealing with Ventura County bail bonds, this matters because speed and paperwork usually pull in opposite directions. A house may offer strong value, but it takes documents. A paid-off vehicle might be faster if the title is clean. Cash is the easiest to confirm. Jewelry may sound helpful but often creates delays because value is harder to pin down.

A lot of stress comes from not knowing what the agent is really asking for. They're not asking for random property. They're asking for security they can rely on if the defendant doesn't appear in court.

That's why fast bail bonds Ventura isn't only about answering the phone at all hours. It's also about telling families, quickly, what's likely to be accepted and what probably won't.

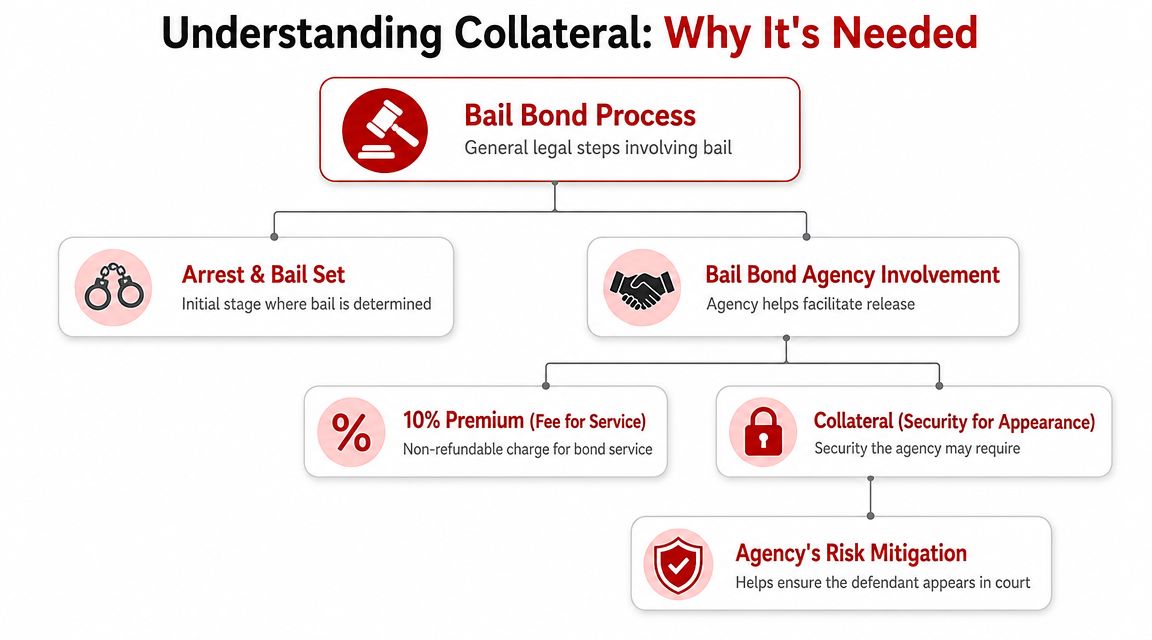

Why Collateral Is Sometimes Required for Bail Bonds

California bail work moves fast, but the financial obligation behind it is real. When a bail bond agency writes a bond, it gives the court a guarantee that the defendant will appear. The family pays the 10% premium, which California law sets as the bond fee. That premium is the cost of the service. It is not the same thing as collateral.

Collateral serves a different purpose. It protects the agency if the defendant disappears and the bond creates a loss.

Why an agency asks for it

Some bonds can be written with the premium and a qualified co-signer alone. Others can't. Large bail amounts, out-of-county ties, prior failures to appear, limited local stability, or a weak indemnitor file can all push the bond into collateral territory.

That request often surprises families because they assume paying the premium finishes the deal. It doesn't always. The premium compensates the agency for writing the bond. Collateral helps secure the risk tied to the defendant's court appearance.

Practical rule: If the agency believes it would face a serious loss after a nonappearance, it may require an asset that can back up the promise made to the court.

The idea isn't unique to bail. In broader finance, collateral can include a wide range of assets. The International Capital Market Association notes that major markets use security such as government and corporate bonds, equities, and even gold, which shows how broadly the concept of valuable assets securing an obligation is used in practice in finance (ICMA on collateral used in repo markets).

What collateral is not

It's not an extra hidden fee. It's not a punishment. It's not a sign that your family member can't be helped.

It's also different from paying full bail directly to the court. If someone pays full bail in cash to the court, that's a separate process from using a bondsman. In a bail bond transaction, the agency posts the bond and may require collateral depending on risk.

For Ventura County Jail bail bonds, the fastest move is usually to ask early whether the bond can be approved with premium only, premium plus co-signer, or premium plus collateral. That question saves time, especially when the defendant is sitting in Ventura, Oxnard, or transferred from another local booking facility.

Assets Commonly Used for Ventura County Bail Bond Collateral

What can be used as collateral in theory is a long list. What gets accepted quickly in Ventura County is a shorter one. In practice, approval usually comes down to three things: liquidity, title clarity, and resale certainty. Consumer banking guidance makes the same point. A home or cash-backed account is generally easier to pledge than collectibles or luxury items with subjective value (Experian on what lenders look for in collateral).

If your family is sorting through options under pressure, this page on bail bond payment options helps organize what's usually workable.

Real estate usually gets the strongest review

Real estate is often the most useful form of collateral for larger bonds. Houses, condos, and some land can work because they're easier to document than personal valuables and usually carry more stable value than movable property.

What matters is not just ownership. It's usable equity and clear paperwork. If the property has heavy loans against it, unresolved title issues, or multiple ownership disputes, it may not help much.

Real estate tends to work best when the family can produce:

- Proof of ownership: deed or other title documents

- Loan information: mortgage statements showing what's still owed

- Basic valuation support: tax records or other current property information

Vehicles can work if the title is clean

A paid-off vehicle is common bail collateral because it's familiar and relatively easy to document. If the pink slip shows clear ownership and the vehicle has enough value, it may be a practical option for fast bail bonds Ventura cases.

A vehicle becomes harder to use when:

- There's still a lender lien: the owner doesn't control the full value yet

- The car is older or damaged: resale certainty drops

- Title records don't match: name issues and transfers can stall approval

For families in Oxnard or Ventura trying to move the process quickly, a clean-title vehicle is usually far more practical than a high-end collectible with uncertain resale value.

Cash and cash backed accounts are the simplest

Cash is the most straightforward collateral because there's no valuation debate. If the funds are available and can be verified, review is usually cleaner than with real estate or personal property.

Some families also have cash-backed accounts or similar assets that are easier to confirm than physical valuables. That doesn't mean every account will qualify. It means cash-like assets are generally easier to review because there's less guesswork.

Jewelry stocks and other valuables are case by case

Families often ask about jewelry, watches, fine art, stocks, or other investments. These can sometimes be considered, but they're less predictable. The problem is usually one of proof, liquidity, and value swings.

Stocks and bonds may look strong on paper, but marketable securities carry a built-in risk because their value can drop after they're pledged. That kind of volatility makes them less dependable than stable property in a fast-moving credit situation. The same practical concern applies in bail underwriting.

Comparing common bail bond collateral types

| Asset Type | Approval Speed | Key Requirement |

|---|---|---|

| Real estate | Moderate | Clear ownership and usable equity |

| Paid-off vehicle | Faster | Clean title and reasonable resale value |

| Cash | Fastest | Verifiable available funds |

| Jewelry or art | Slower | Reliable appraisal and resale certainty |

| Stocks or bonds | Case by case | Verifiable ownership and tolerance for value changes |

A family may own something valuable but still not own something usable. In bail collateral, those are two different things.

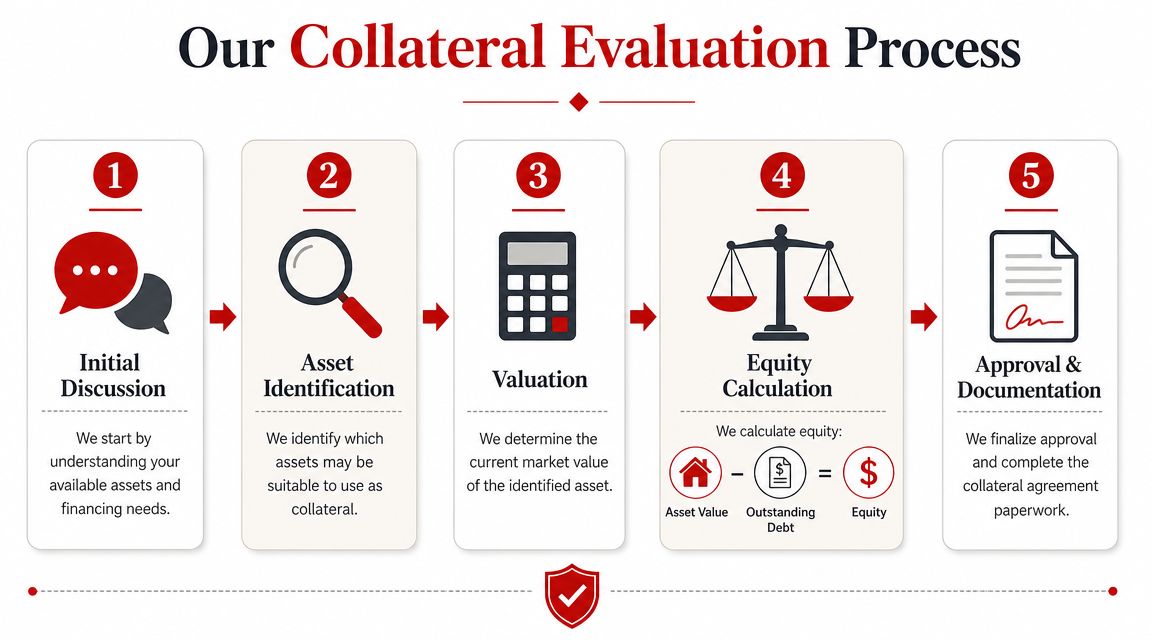

How We Evaluate and Approve Your Collateral

Families usually think the review starts with the asset type. It starts with the numbers behind ownership. A house, car, or account only helps if the owner can show enough value remains after debts and liens are accounted for.

That's why collateral review is usually faster when the family stops trying to guess what matters and just gathers documents right away. For people handling Ventura County bail bonds in a hurry, that can save hours.

The first question is equity

The key issue is equity, not just ownership. A basic lending rule applies here too. An asset must have sufficient equity and clear title, because a borrower can't fully pledge value they don't own outright. Banking guidance makes this point directly and notes that an asset already heavily encumbered by another claim may be rejected (North Shore Bank on why equity and title matter in collateral).

In plain language, the review often looks like this:

- Identify the asset: house, vehicle, account, or another item.

- Confirm ownership: whose name is on the title, deed, or statement.

- Check for liens or loans: what's still owed.

- Estimate current value: enough to judge practical security.

- Measure usable equity: value minus debt.

A family member may say, “I own the car.” If the lender still has a lien and most of the value is tied up, that car may not solve the bond problem.

What documents usually speed things up

Different assets need different proof, but a few items come up repeatedly.

- For real estate: deed, mortgage statement, recent property tax information, and ID for the owner.

- For vehicles: title or pink slip, registration, payoff information if there's still a loan, and ID.

- For bank or investment assets: current statements and proof the account holder has authority over the asset.

- For co-signed deals: financial information for the indemnitor and paperwork showing ability to support the bond.

If you're also trying to understand who carries legal responsibility after release, this guide on how co-signing a bail bond works lays out the obligations in plain English.

Bring more paperwork than you think you need. Missing documents usually delay release more than the asset choice itself.

The goal of review isn't to make the process harder. It's to avoid writing a bond against property that can't be enforced if something goes wrong.

Safeguarding and Recovering Your Pledged Assets

The biggest fear most families have is simple. If we put up collateral, are we going to lose it?

Usually, no. In the normal course of a case, the defendant goes to court as required, the bond is eventually exonerated, and the pledged collateral is released back to the owner. The asset doesn't become the agency's property just because it was used to secure the bond.

What puts collateral at risk

Collateral is at risk when the defendant fails to appear and the problem isn't fixed within the court process. That can trigger forfeiture issues tied to the bond. Every case has its own timeline and legal details, but the practical point is straightforward. The asset becomes relevant only if the bond obligation goes bad.

This is one reason stable assets are preferred over volatile ones. Consumer lending guidance notes that financial assets like stocks or bonds can lose value after they're pledged, and a lender may then demand more collateral or reject the asset category for that reason (Rocket Mortgage on the volatility risk of investment collateral).

For bail purposes, that means families should think beyond “Do we own it?” and ask “Will this still hold up if the case drags on?”

How collateral is returned after the case

Once the court's obligation ends and the bond is exonerated, the collateral release process can move forward. For document-based collateral, that usually means the title, deed paperwork, or recorded security documents are returned or released according to the agreement.

The cleanest path to getting collateral back is boring but important:

- Make every court appearance: missed dates create avoidable problems.

- Stay reachable: if the defendant moves or changes phone numbers, update the agent.

- Keep copies of everything: agreements, receipts, titles, and signed forms.

- Ask when exoneration is expected: don't assume the bond ends the day the case feels “done.”

If you're trying to sort out the difference between premium payments and money that may be returned later, this guide on whether you get bail money back in California clears up that common confusion.

Most collateral problems don't start with the asset. They start with missed court.

No Collateral? Other Options for Securing a Bond

The call usually sounds the same. A husband, parent, or sister says they can help, but they do not own a house free and clear, the car still has a loan, and they are worried that means their loved one has to stay in jail.

In Ventura County, that is not unusual. A lot of families can handle the responsibility of a bond but do not have the kind of asset that is easy to pledge on short notice. What matters is whether the file can still be approved through income, a qualified co-signer, partial security, or a workable payment arrangement.

The practical question is simple. What will get this bond written fastest, with the least risk to the family?

Payment plans and co signers can solve the problem

Collateral is only one way to reduce risk on a bond file. In real cases, especially around Ventura, Oxnard, Santa Paula, Moorpark, Ojai, Fillmore, Port Hueneme, Thousand Oaks, and Santa Barbara, I often see approvals depend more on the full picture than on one asset alone.

That full picture can include:

- A qualified co-signer: steady income, valid ID, local ties, and a record that shows they can take responsibility if problems come up

- A payment plan for the premium: useful when the family has income but cannot put all the money together the same day

- A mixed file: a smaller asset, plus proof of income and a strong indemnitor, can sometimes work better than waiting on one larger asset

- Better documentation: pay stubs, bank activity, proof of residence, and reachable references can make the decision easier

Local agencies like Bada Bing Bail Bonds often provide payment plans, co-signer options, and collateral solutions depending on the bond amount and file review.

If the main problem is timing, not willingness to pay, some families also review options for loans for bail bonds before they decide how to cover the premium.

A quick overview can help before you call:

What to ask on the first call

A stressed family member will often ask only one thing. “How much is it?” That is understandable, but it is not enough to tell you whether release can happen tonight.

Ask these instead:

- Can this bond be approved with a co-signer and income verification only

- If some security is needed, what is the fastest acceptable option

- What documents should I send right now to avoid delay

- If I do not own property, what other approval paths are realistic on this file

- How quickly can you review the co-signer and paperwork once I send it

Those answers save time. They also keep families from scrambling for assets they do not need, or offering property that will never be accepted on this type of bond.

Frequently Asked Questions About Bail Bond Collateral

Can I use a car that still has a loan on it

Sometimes, but the loan matters. What counts is the remaining equity after the payoff amount is considered. If the vehicle is nearly paid off and the title situation is clean, it may still help. If there's little equity left, it may not.

Can family members combine collateral

Yes, that can happen in some cases. One person might provide the co-signer role, while another provides a vehicle, account support, or property documents. The key issue is whether each person's ownership and responsibility can be documented clearly.

Does collateral have to be in Ventura County

Not always. Property outside Ventura County can sometimes be considered, but distance can slow verification and paperwork. For urgent Ventura County Jail bail bonds, local assets are often easier because records and signatures may be faster to coordinate.

What if the defendant misses court

That creates the main risk behind any collateral agreement. The family should contact the bail agent immediately. Waiting usually makes the situation harder. A missed appearance doesn't always mean the collateral is gone, but it does put the bond in danger and can trigger serious follow-up steps.

Can I use jewelry or collectibles

Possibly, but they're less dependable. The issue usually isn't whether they have personal value. It's whether the item has a value that can be verified and relied on if the asset ever had to be sold.

Will I get my collateral back when the case ends

If the bond is properly resolved and the court exonerates it, the collateral is generally released according to the agreement. Families should keep copies of all signed documents and ask what final paperwork will confirm release.

What should I have ready before I call

These items usually help:

- Defendant details: full name, date of birth if available, and where they're booked

- Case basics: charges if known and any booking or bail information

- Asset paperwork: title, deed, statements, or payoff information

- Co-signer information: ID, contact info, employment, and address history if requested

For families dealing with bail bonds Oxnard, fast bail bonds Ventura, or a late-night booking anywhere in Ventura County, the best next step is a direct call with the facts you have. You don't need to solve the whole collateral question before you reach out. You do need to get the review started.

If you need straight answers right now, contact Bada Bing Bail Bonds. A licensed agent can review the booking, explain whether collateral is likely, tell you what documents will help most, and walk you through practical options for Ventura, Oxnard, Camarillo, Port Hueneme, Thousand Oaks, Santa Paula, Moorpark, Fillmore, Ojai, Santa Barbara, and surrounding Southern California areas.