The call usually comes late. A son, husband, daughter, or friend has been arrested somewhere in Southern California, nobody understands the paperwork, and the first question is simple: What does a surety bond mean, and what do we need to do right now?

In bail, that question isn’t academic. It decides who signs, who pays, what risk the family is taking on, and how fast release can happen. If you’re trying to get someone out of jail, the legal language can sound colder than the moment feels. The good news is that the concept is simpler than it sounds once you strip away the jargon.

Table of Contents

- What Is a Surety Bond? The Three-Party Promise

- How a Surety Bond Differs from an Insurance Policy

- Common Types of Surety Bonds and Their Uses

- Understanding Bail Bond Costs in California

- How to Get a Bail Bond Step-by-Step

- Practical Answers to Urgent Bail Bond Questions

What Is a Surety Bond? The Three-Party Promise

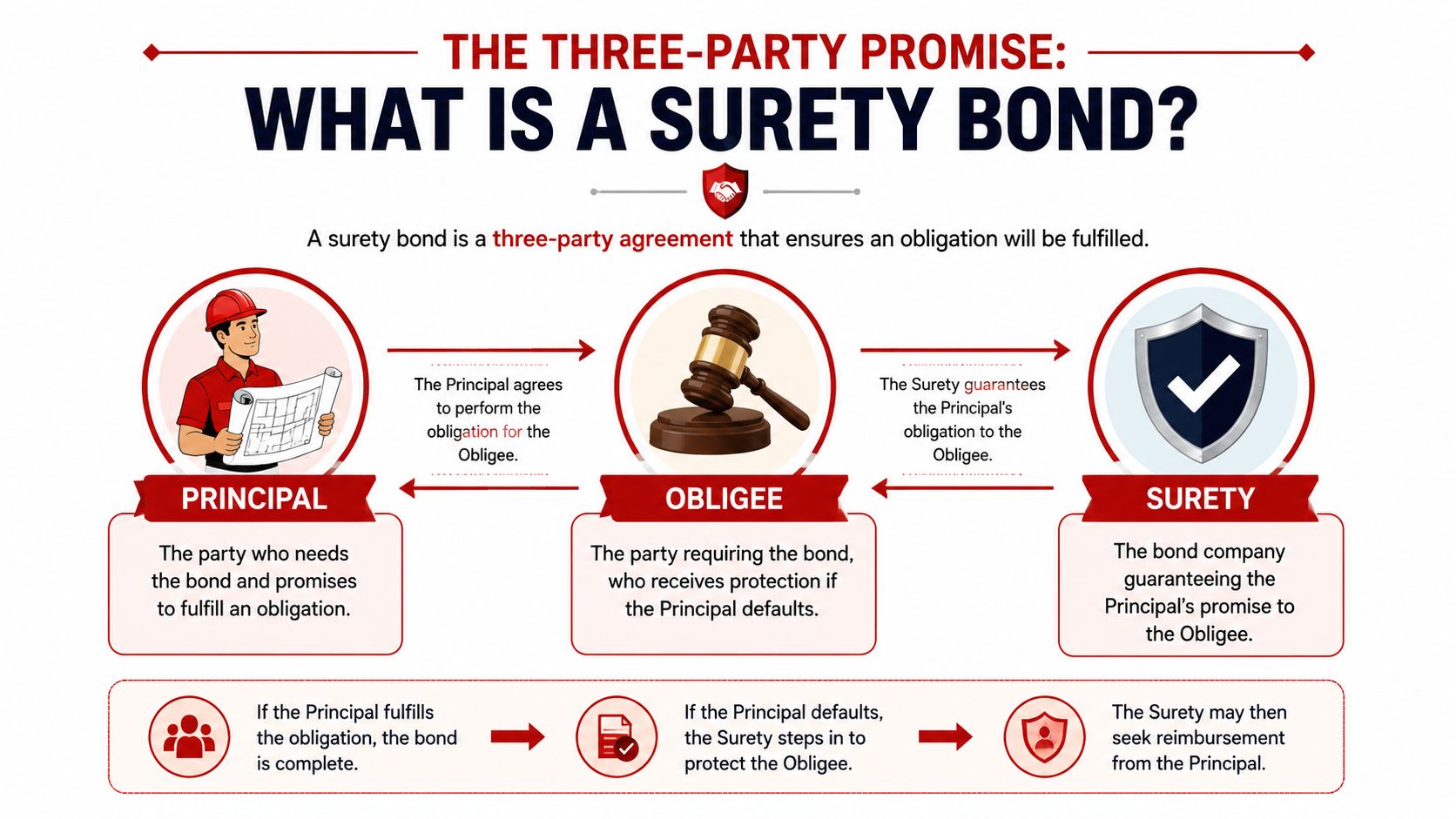

A plain-English answer is typically sought for the surety bond meaning. In bail, a surety bond is a legal promise backed by money and paperwork. One party needs to meet an obligation, another party demands protection, and a third party guarantees that obligation will be honored.

A surety bond is a three-party promise. If the person who must comply doesn’t do it, the guarantor can be held financially responsible.

Who each party is in a bail case

It’s akin to a serious co-sign, not a favor between friends.

In a surety bond, the principal is the person who must do something. In a bail case, that means the defendant must appear in court and follow the release conditions. The obligee is the party requiring protection. In bail, that’s the court. The surety is the company that guarantees the obligation.

If you want a quick primer on the bail side of the process, What is bail gives the basic court context.

A simple way to picture it:

| Party | In general | In a California bail case |

|---|---|---|

| Principal | The one who must perform | The defendant |

| Obligee | The one requiring protection | The court |

| Surety | The one guaranteeing the promise | The bail bond company |

Why this promise carries legal weight

This isn’t casual paperwork. It’s a standardized legal instrument. As Nationwide’s explanation of surety bonds notes, a surety bond is built on a three-party structure involving the principal, obligee, and surety, and federal surety bonding is administered by the U.S. Bureau of the Fiscal Service under 31 U.S.C. 9304-9308. It also notes that Department Circular 570 was updated on July 1, 2024 to list approved companies that may write or reinsure federal bonds.

That federal framework matters because it shows what a surety bond really is. It’s not a handshake. It’s not a loose promise that people hope will hold up. It’s a recognized financial guarantee used across construction, licensing, procurement, and court-related settings.

Practical rule: In a bail case, the court isn’t asking whether the family means well. The court wants a financial guarantee that the defendant will return.

That’s the core of surety bond meaning in practice. The bond exists to satisfy the court’s demand for accountability so the defendant can be released before the case is finished.

How a Surety Bond Differs from an Insurance Policy

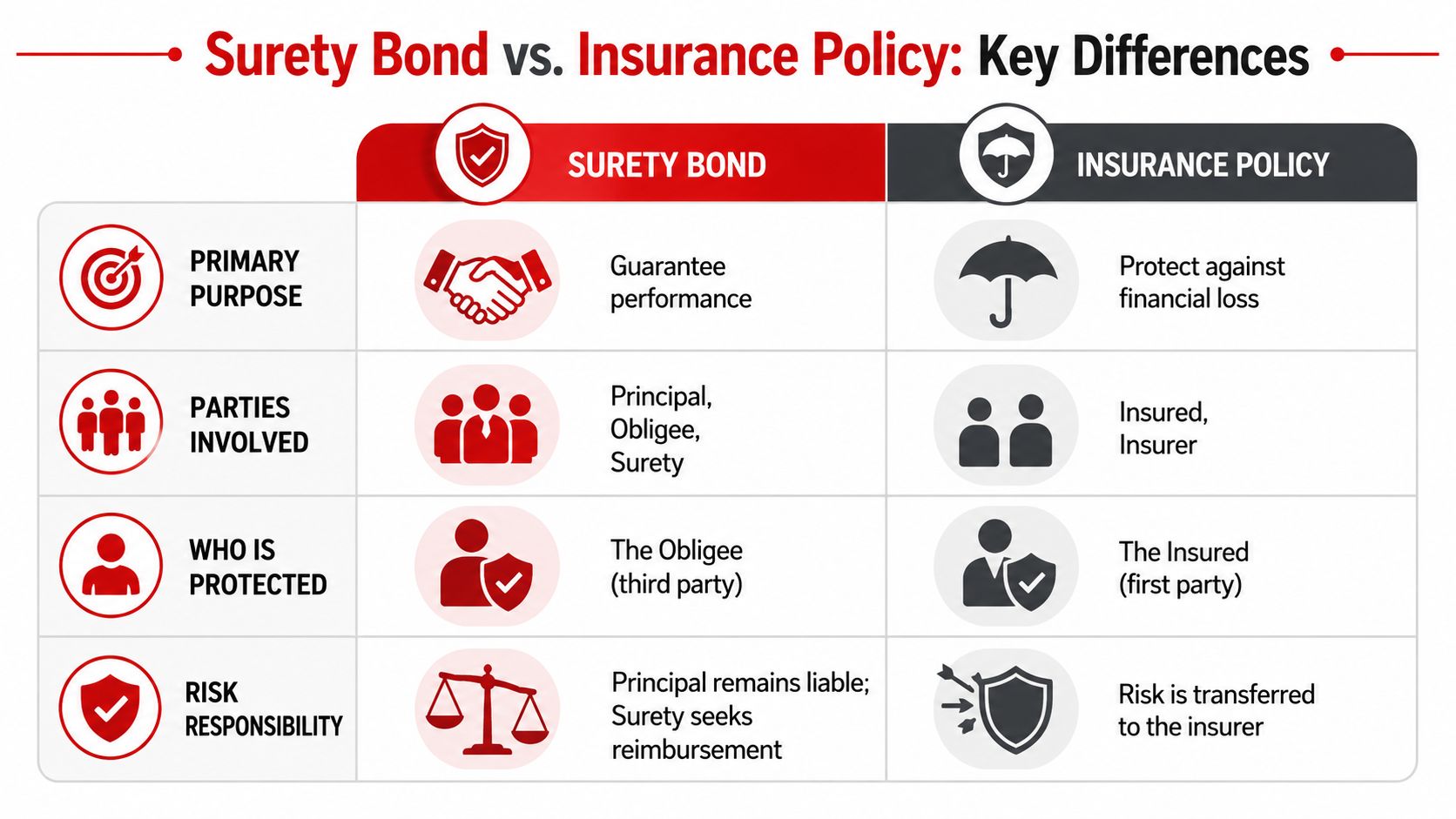

Families mix these up all the time, especially when they’re scared and moving fast. They hear “bond company” and assume it works like car insurance or homeowner’s insurance. It doesn’t.

A surety bond and an insurance policy may both involve a company, a premium, and a claim process. That’s where the similarity ends.

The mistake families make under stress

You might think, “We pay the fee, so the bond company takes the risk from there.”

In reality, that’s not how a surety bond works. A surety bond is a three-party guarantee, not a product built to absorb expected loss the way insurance does.

Here’s the side-by-side difference:

- Insurance protects the policyholder. If a covered loss happens, the insurer is taking on that risk under the policy terms.

- A surety bond protects the obligee. In bail, the obligee is the court, not the family.

- Insurance transfers risk. A surety bond backs a promise and expects compliance.

- A bond claim doesn’t erase responsibility. The underlying obligation still matters.

Who ultimately pays if something goes wrong

The cleanest way to understand this comes down to one question: who ends up holding the bill if there’s a valid claim?

As Wall Street Prep’s explanation of surety bond meaning states, a surety bond is different from insurance because the principal must reimburse the surety for valid claims, so it isn’t a risk-transfer product like insurance. That source also frames the practical question the right way: “If a claim is paid, who ultimately pays?”

That question matters a lot in bail.

If the defendant skips court, the problem doesn’t disappear because a bond was posted. The bond was the guarantee. It got the person released. It did not replace the person’s duty to appear.

Families do best when they treat a bail bond like a credit-backed promise to the court, not like coverage that wipes out the consequences of missing court.

That’s why co-signers need to slow down long enough to understand what they’re signing. In a panic, people focus on getting their loved one out. They should. But they also need to understand the obligation they’re stepping into. A bail bond solves the immediate custody problem. It does not remove the duty to show up and finish the case properly.

Common Types of Surety Bonds and Their Uses

Surety bonds show up in more places than one might expect. Once you know that, the term stops feeling mysterious. Bail bonds are urgent, but they’re not unusual in the larger financial and legal system.

Where most people encounter surety bonds

Some surety bonds support construction projects. A contractor may need a bond before bidding or before starting work. Other surety bonds support licenses and permits. A business owner may need one to satisfy a state, city, or regulatory requirement before operating.

The broader market is large. The U.S. Small Business Administration reported that its Surety Bond Guarantee Program reached $10.6 billion in guarantees in fiscal year 2025, supporting bonds for contracts and subcontracts up to $9 million. That same source says the overall U.S. surety market was just under $7 billion in written premium in 2020.

Those numbers tell you one important thing. Surety bonds are not fringe paperwork. They’re a common tool used to back legal and financial obligations across the economy.

If the arrest involves impaired driving, this DUI bail bond guide can help put the bail side of things in context.

Why bail bonds fit inside the larger surety world

Court-related bonds are part of that same surety framework. In practical terms, bail bonds sit in the judiciary side of the bond world because the obligation is tied to a court process.

That matters for families because it changes how you should think about the transaction. You’re not buying freedom. You’re arranging a lawful guarantee so the court will release the defendant while the case is pending.

A few common categories look like this:

- Contract bonds support performance on projects.

- License and permit bonds support compliance with business rules.

- Court bonds support obligations tied to legal proceedings.

- Bail bonds deal with pretrial release and court appearance.

When a family hears “surety bond,” they often think it sounds abstract. In a bail case, it’s just the court-approved mechanism that allows release while the case moves forward.

That’s the useful bridge. The legal structure is broad, but the immediate application is personal. In Southern California, the bond is the tool that gets a person out of custody while keeping the court protected.

Understanding Bail Bond Costs in California

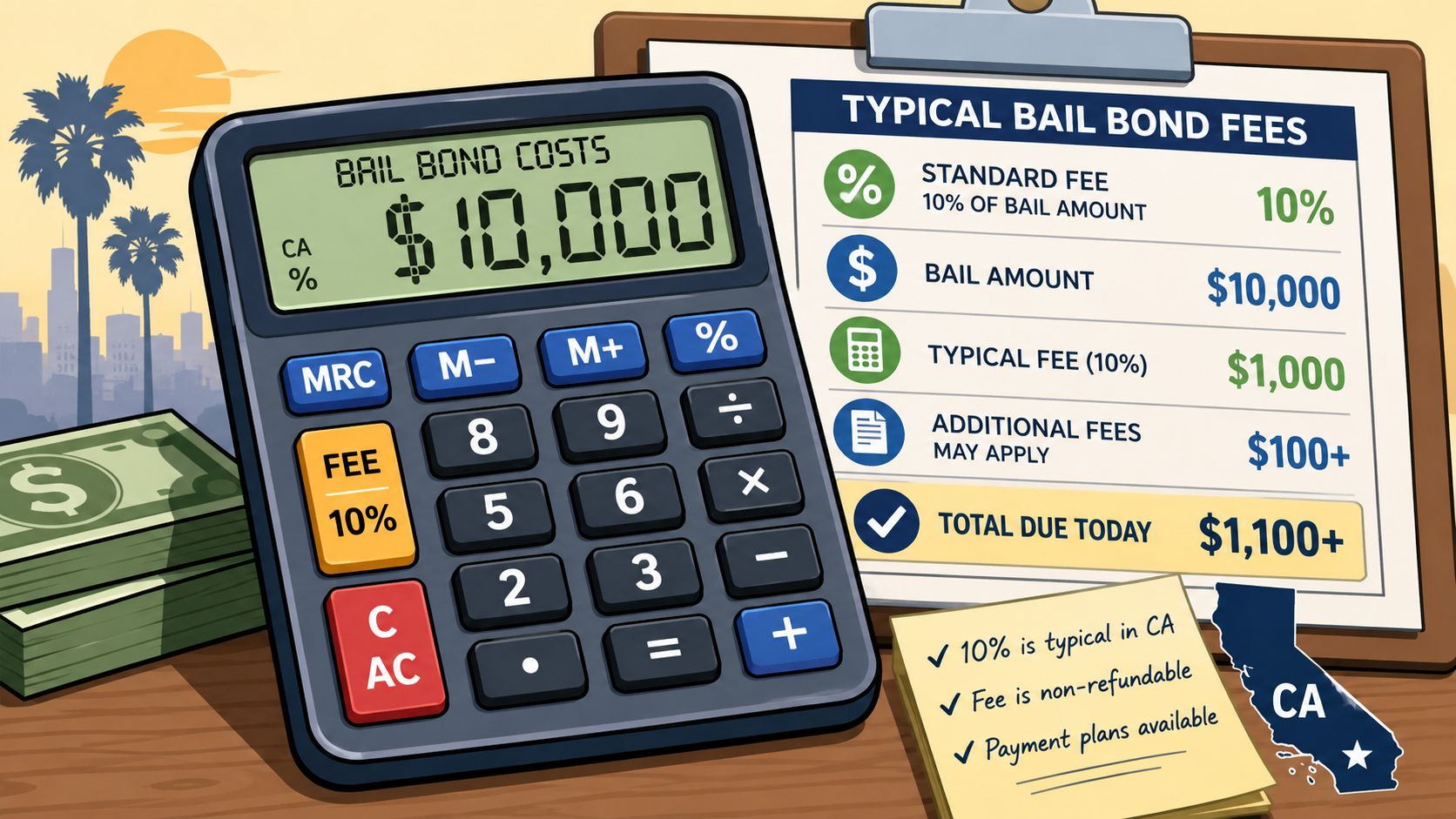

Cost is usually the second question after “Can you get them out?” The first thing to understand is that a bail bond premium is tied to the total bail amount, but the bond company also has to evaluate risk before agreeing to write the bond.

What affects the premium

In the wider surety market, pricing is commonly a small percentage of the total bond amount, with premiums often ranging from 0.5% to 10%, and the rate depends on bond size, risk level, and the applicant’s financial history, according to SuretyBonds.com’s overview of surety bond pricing.

In California bail practice, families also need to understand the local rule that matters most: the publisher states that bond premiums are set by law at 10% of the total bail in California. That gives families a clearer starting point when they’re trying to estimate cost fast.

The premium is only part of the decision, though. Approval depends on whether the bondsman believes the defendant will appear and whether the co-signer can stand behind the obligation.

A bondsman typically looks at things like:

- The charge itself. Some cases present more appearance risk than others.

- Local ties. Work, family, housing, and roots in the area matter.

- Court history. Prior failures to appear can raise concern.

- The co-signer’s strength. Stability, income, and reliability affect the file.

- Bond size. Larger bonds often require more documentation and, sometimes, collateral.

What a bondsman will ask you for

Families often lose time because they call without the basics. The fastest approvals usually happen when the caller has the key details ready.

Expect questions such as:

-

Who was arrested

Full legal name matters. Nicknames slow verification. -

Where they are being held

Jail location changes the posting process. -

What the bail amount is

If you don’t know it yet, an agent may help verify it. -

Who will co-sign

The co-signer is part of the risk review, not just the payment source. -

Whether collateral may be needed

This comes up more often on larger or riskier files.

For a fuller explanation of the mechanics, this guide on how bail bonds work in California walks through the release process in practical terms.

Reality check: The cheapest-looking conversation is not always the fastest one. Speed comes from accurate information, a qualified co-signer, and a realistic understanding of the risk.

What works is being organized and honest. What doesn’t work is hiding facts, guessing at the booking information, or assuming every bond can be approved with the same terms.

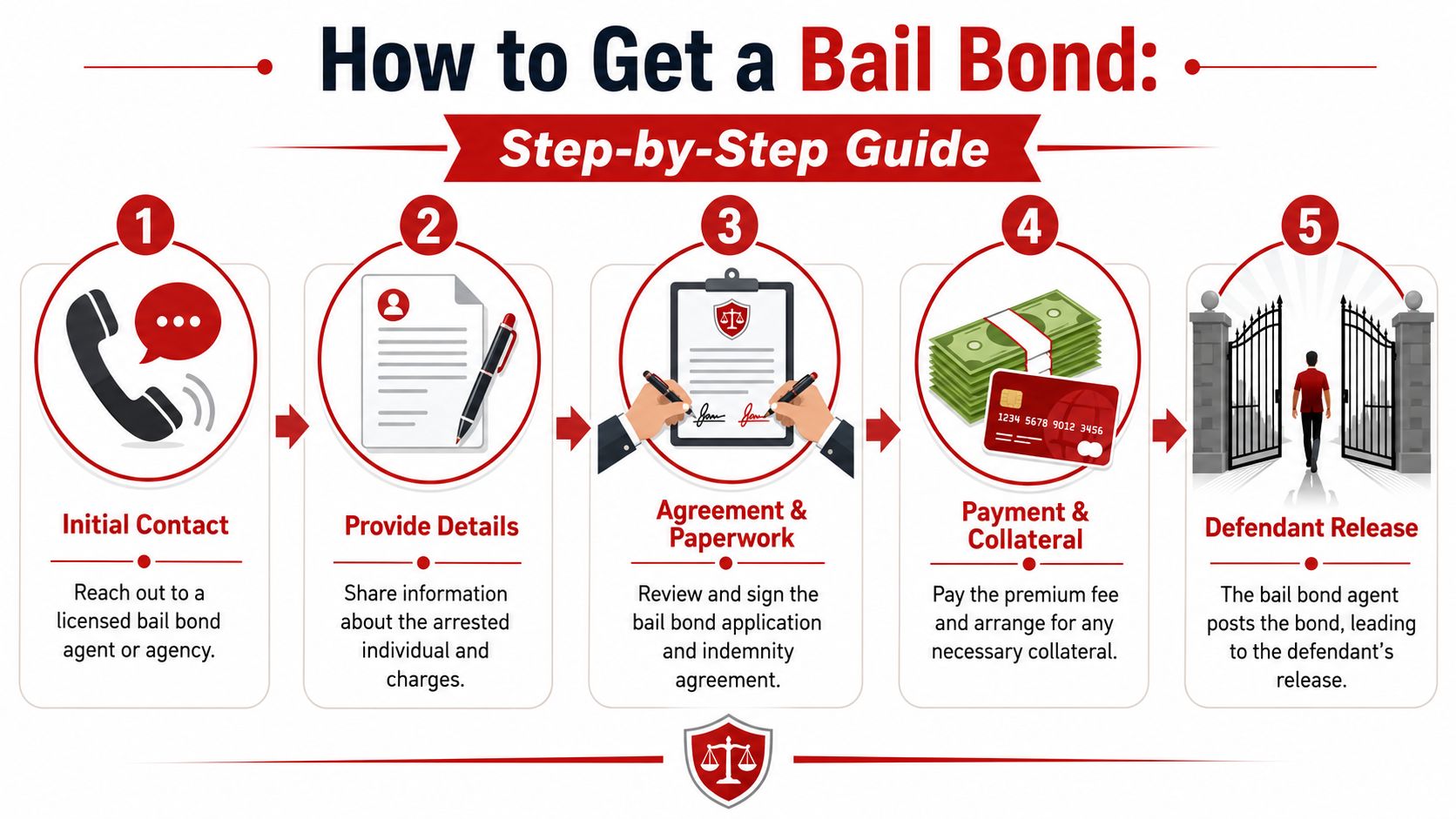

How to Get a Bail Bond Step-by-Step

A 2 a.m. jail call usually comes with half the facts, a lot of panic, and one question. How do we get them out fast? In Southern California, the answer is usually simple on paper and stressful in real life. The families who move quickest focus on the next step, not the whole case at once.

The fastest path from phone call to release

-

Call a licensed bail bond agent right away

Start with the basics you have now. Full legal name, jail or city of arrest, date of birth if you know it, and any booking number or case details. If some of that is missing, call anyway. A good agent can start checking. -

Verify that the person is booked and confirm the bail

This is the first real checkpoint. If the jail has not finished booking, the bond cannot be posted yet. Families often lose time here because they were given incomplete or wrong information during the first phone call. -

Go over the terms before you sign

Ask what the premium is, who will be the co-signer, whether collateral is required, and what could slow approval. This is the practical side of surety bond meaning. The bondsman guarantees the bond to the court, and the co-signer promises to stand behind that obligation if the defendant does not appear.

A practical explainer can help if you need a quick visual walkthrough:

-

Sign the paperwork and handle payment

This part moves fast if the co-signer is ready. Have photo ID available. Be ready to provide address details, employment information, and anything else the agent needs to write the bond file correctly. -

The bond gets posted with the jail or court

After that, release is mostly on the jail’s clock, not yours. Some facilities move quickly. Others do not, especially during shift changes, busy booking periods, or if there are other holds. -

Stay by the phone until the person is released

Release times are not always predictable. People are often let out with very little notice and need a ride, a phone, or instructions about their next court date.

If you need a faster walkthrough focused on immediate action, this guide on how to bail someone out fast keeps the process tight and practical.

What slows the process down

Posting the bond is only one part of the job. The jail still controls release processing, and that catches families off guard.

Common delays include:

- Incomplete booking. The jail has not fully entered the arrest yet.

- Wrong identifying details. A misspelled name, wrong birth date, or wrong facility can waste a lot of time.

- Co-signer problems. Missing ID, missed calls, or inconsistent information can stall approval.

- Collateral review. Larger or riskier bonds sometimes need extra documentation before the bond is written.

- Other holds. Immigration holds, probation issues, or warrants from another court can delay release even after the bail bond is posted.

One more point matters. Fast service does not always mean instant release. A bondsman can speed up verification, paperwork, and posting. The jail still decides when the door opens.

The families who get through this fastest are usually the ones who stay reachable, answer questions clearly, and send documents as soon as they are requested.

Practical Answers to Urgent Bail Bond Questions

Much of the apprehension stems from this situation. Families usually understand the idea of the bond by this point. What they still need are straight answers about risk, timing, and what happens if something goes wrong.

Collateral and missed court dates

What is collateral?

Collateral is property or value pledged to secure the bond obligation. A bondsman may ask for it when the bail is large, the risk looks higher, or the co-signer’s financial profile doesn’t fully support the bond on its own.

Do you get collateral back?

Usually, collateral is tied to successful completion of the bond obligation. If the defendant appears as required and the bond is properly exonerated at the end of the case, collateral is generally returned according to the agreement. The key is to read the paperwork and keep copies.

What happens if the defendant misses court?

This is the question families should ask before signing, not after.

As Jurisco’s explanation of surety bonds states, a surety bond is a three-party financial guarantee involving the principal, obligee, and surety. If the principal defaults, the surety pays valid claims and then seeks reimbursement from the principal. That same structure is what makes a co-signer financially responsible if a defendant fails to appear in court.

That means a missed court date can become everyone’s problem quickly. The defendant may face additional legal trouble. The co-signer may face financial exposure. The bond company may try to locate the defendant and resolve the default before losses harden into a full claim situation.

If the defendant misses court, silence is the worst move. Call the lawyer and the bond agent immediately. The sooner the problem is addressed, the more options usually remain.

Release timing and co-signer concerns

How long does release take after the bond is posted?

There isn’t one universal answer because the jail controls the release line, staffing, internal checks, and discharge procedures. In practice, release can move quickly at one facility and drag at another. Nights, shift changes, medical holds, and heavy booking volume can all affect timing.

What helps is making sure the bond side is clean. Accurate defendant information, a reachable co-signer, signed paperwork, and prompt payment remove the avoidable delays.

Do you need good credit to co-sign a bail bond?

Not always in the way people think. A bondsman is looking at the whole file, not just one number. Stable employment, a long residence history, family connection to the defendant, and willingness to provide documents can matter. If the file carries more risk, the bondsman may ask for collateral or another co-signer.

Can more than one person help on the bond?

Sometimes, yes. On harder files, families may combine resources. One person may handle payment. Another may help support the indemnity side. The exact structure depends on the agent’s underwriting decision and the facts of the case.

What should the co-signer do after release?

Stay involved. Make sure the defendant has court dates, transportation, a working phone, and a plan. Most bond problems don’t start with bad intentions. They start with chaos, avoidance, missed reminders, or substance issues nobody wants to confront early.

A practical next step is to review Surety Bail Bonds FAQ, especially if you’re weighing whether to co-sign.

What works best after release?

- Keep every document. Save receipts, agreements, and court information.

- Confirm court dates directly. Don’t rely on memory or secondhand updates.

- Stay in contact with the defendant. Distance creates risk.

- Tell the agent about problems early. Missed rides, relapse, confusion, or fear should be addressed before a court date is missed.

The plainest understanding of surety bond meaning in a California bail case is this: the court allows release because a surety stands behind the defendant’s promise to return, and the family often stands behind that surety with a signed financial commitment.

If you need immediate help with a Southern California bail bond, Bada Bing Bail Bonds provides 24/7 assistance, explains the paperwork in plain English, verifies booking details, and helps families move from panic to a clear release plan.